by Yair Kaldor*

The growing size and importance of financial markets, institutions, and activities—often labeled as “financialization”—is one of the key economic developments of recent decades. The rise of finance coincides with a long period of increasing income inequality across advanced economies, evident in rising GINI coefficients, a decline in the labor share of national incomes, and growing disparities between top corporate managers and the average workers. In recent years economic sociologists and political economists have devoted much-needed attention to the relationship between these developments and provided increasing evidence of a strong statistical association between indicators of financialization and income inequality at different levels of analysis.

Although this emerging literature recognizes that it is labor that ends up paying the price of financialization through stagnant wages and increased job insecurity, workers themselves remain conspicuously silent in existing accounts. Rather than the struggle between labor and capital, these studies focus mainly on the conflict between managers and shareholders or the subordination of production to finance. As a result, the impact of financialization on income inequality appears at most as an unintended consequence or unfortunate side-effect, and it remains unclear where workers were when all of this was taking place.

In an article titled “Financialization and income inequality: bringing class struggle back in”, recently published in Critical Sociology, I offer a different perspective on the issue by exploring both financialization and income inequality from within the historical development of the class struggle between labor and capital. Focusing on the United States, where financialization first became evident and where it has advanced the most, the article traces the historical roots of this development to the late 1960s and the decline of the long economic expansion that followed World War II, often considered as “the golden age of capitalism”. While many scholars view financialization as a response to the economic problems that persisted through the 1970s—including a crisis of corporate profitability and high levels of inflation—the article shows that these problems themselves were closely related to the escalating class conflicts during the period. Viewed from this perspective, the impact of financialization on income inequality appears less as an unintended consequence and more as its very raison d’etre.

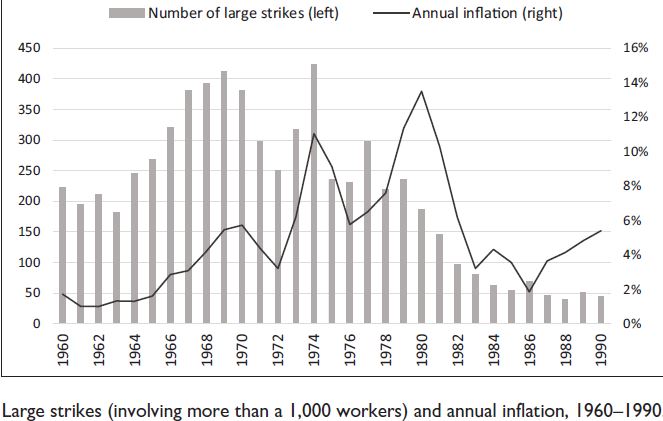

The article challenges some of the common assumptions regarding financialization, including the importance of the shareholder value model and the growing power of a rentier class. It shows that when faced with a slowdown in growth and increased international competition, corporate managers hardly sat idle while waiting for a new model of corporate governance to emerge. Instead, they tried to increase the productivity of workers while holding down their wages. However, the militancy of rank-and-file union leaders that emerged with the full employment of the mid-1960s proved effective in thwarting these efforts. The mobilization of organized labor played an important role in driving up consumer prices in the following years, a trend that was exacerbated by loose monetary policies and the oil crisis of 1973. The inflation that persisted throughout the decade was not unwelcomed by large American nonfinancial corporations, as it inflated their profit rate by devaluing the assets on their balance sheet and improved their competitiveness on the global market. However, inflation posed a major problem for financial institutions and investors, as it depressed prices on the stock exchange and eroded the value of outstanding loans.

By the end of the decade, the risk of inflation was driving many away from the corporate bond market, forcing nonfinancial corporations to rely more heavily on short-term finance and making it harder to continue recycling their debts. This created the basis for a cross-sectorial alliance between industry and finance, which was united in the conclusion that to bring inflation under control it is necessary to break the power of organized labor in the United States. The appointment of Paul Volcker as chair of the Federal Reserve, the “Volcker Shock”, which for many marks the beginning of the neoliberal era and a decisive moment in the rise of finance, and the resounding defeat of organized labor during the economic recessions that followed this U-turn in monetary policy, must be understood as the outcomes of the earlier developments reviewed above.

The article contributes to our understanding of financialization and income inequality by incorporating insights from existing studies within a broader framework that prioritizes the class struggle between labor and capital over the conflict between managers and shareholders or finance and industry. By investigating the economic turmoil of the 1970s from a class perspective, it brings the relationship between financialization and income inequality closer to the surface. No less important, this class struggle framework restores to labor the agency which is largely denied from it in existing accounts. Rather than being innocent victims of developments they have nothing to do with, the article shows that the financialization of the American economy was only accomplished after fierce battles, as workers and their unions fought to protect the gains achieved during the postwar era. That these battles ended in the defeat of organized labor should not lead us to ignore them, or assume that financialization automatically reduced the wages of workers without any response. In other words, the article suggests that the impact of financialization on income inequality should be viewed as a contingent outcome of the historical development of the class struggle.

—————–

* Yair Kaldor is a sociologist and political economist. He is currently a postdoctoral researcher at the Department of Sociology at the University of Haifa. His research focuses on the relationship between financialization and the decline of organized labor, the growing importance of financial assets as a form of private property, and the legal foundations of the shift toward finance.

***

Join Economic Sociology & Political Economy community via

Facebook / Twitter / LinkedIn / Whatsapp / Instagram / Tumblr / Telegram

Discover more from Economic Sociology & Political Economy

Subscribe to get the latest posts sent to your email.

The fortunes of the corporate/capitalist elite depend on keeping the workers “over a barrel”.

Marx saw the conflict between those that own the means of production and those who sell their labour as crucial to the maintenance of capitalism. Its function is to create an obedient, docile, uncritical workforce who will work to support the upper-class’s lifestyle and the economy.

That conflict has always been there and came back with a vengeance in 1980!

Financialisation is the latest from the conservative tool kit. Keeping wages low, or debt pressure high, means workers will be less likely to complain or make demands. As workers struggle to provide their families with all the temptations that a capitalist society offers, they become far less likely to risk their employment, and less able to improve their situation.

At bottom, conservatives believe in a social hierarchy of “haves” and “have nots”. They have taken this corrosive social vision and dressed it up with a “respectable” sounding ideology which all boils down to the cheap labour they depend on to make their fortunes.

The larger the labour supply, the cheaper it is. The more desperately you need a job, the cheaper you’ll work, and the more power those “corporate lords” have over you.

Cheap-labour conservatives don’t like social spending or our “safety net”. Why? Because when you’re unemployed and desperate, corporations can pay you whatever they feel like – which is inevitably as little as possible. You see, they want you “over a barrel” and in a position to “work cheap or starve”.

LikeLike

Here, in the States, it strikes me that it’s more about ownership of resources & infrastructure.

It used to be that communities owned a lot of resources & infrastructure in common – grazing land, town forests. Water supplies are still mostly municipal, while some communities still have municipal & cooperative electric utilities – many built during the New Deal era. Unfortunately, outside of those with local hydropower, they mostly have to purchase fuel/power from outside sources.

It strikes me that the need to electrify the world’s power systems provides a wonderful opportunity to rebuild the energy commons – with solar & wind sources generating income to communities-as-a-whole, rather than being a drain.

Rather than talking about owner-worker conflicts – we ALL need to start thinking & acting as owners, not serfs.

LikeLike

Very interesting! Thanks! This article is complementary

https://mondediplo.com/2021/01/10uk

LikeLike

[…] Reframing Financialization: Bringing Class Struggle Back In (by Yair Kaldor, November 21, […]

LikeLike